- Home

- YOUR FUTURE

- Futurist Keynotes

- FUTURE EVENTS

- How Patrick Dixon will transform your event as a Futurist speaker

- How world-class Conference Speakers always change lives

- Keynote Speaker: 20 tests before booking ANY keynote speaker

- How to Deliver World Class Virtual Events and Keynotes

- 50 reasons for Patrick Dixon to give a Futurist Keynote at your event

- Futurist Keynote Speaker - what is a Futurist? How do they work?

- Keys to Accurate Forecasting - Futurist Keynote Speaker with 25 year track record

- Reserve / protect date for your event / keynote booking today

- Technical setup for Futurist Keynotes / Lectures / Your Event

- Dr Patrick Dixon

- Futurist Books

- Clients

- CONTACT for KEYNOTES

Patrick Dixon - Futurist Keynote Speaker "LIFE WITH AI" - 18th book in shops soon

25 Years Experience in Future Trends Forecasting >400 Global Clients - Every Industry and Region

Future of Artificial intelligence - discussion on AI opportunities and Artificial Intelligence threats. From AI predictions to Artificial Intelligence control of our world. What is the risk of AI destroying our world? Truth about Artificial Intelligence

Future of Sales and Marketing in 2030: physical audience of 800 + 300 virtual at hybrid event. Digital marketing / AI, location marketing. How to create MAGIC in new marketing campaigns. Future of Marketing Keynote Speaker

TRUST is the most important thing you sell. Even more TRUE for every business because of AI. How to BUILD TRUST, win market share, retain contracts, gain customers. Future logistics and supply chain management. Futurist Keynote Speaker

How to make virtual keynotes more real and engaging - how I appeared as an "avatar" on stage when I broke my ankle and could not fly to give opening keynote on innovation in aviation for. ZAL event in Hamburg

"I'm doing a new book" - 60 seconds to make you smile. Most people care about making a difference, achieving great things, in a great team but are not interested in growth targets. Over 270,000 views of full leadership keynote for over 4000 executives

Futurist Keynote Speakers - how Futurist Keynotes transform events, change thinking, enlarge vision, sharpen strategic thinking, identify opportunities and risks. Patrick Dixon is one of the world's best known Futurist Keynote Speaker

Futurist Keynote Speaker: Colonies on Mars, space travel and how digital / Artificial Intelligence / AI will help us live decades longer - comment before keynote for 1400 at Avnet Silica event

Future of Travel and Tourism post COVID. Boom for live experiences beyond AI. What hunger for "experience" means for future aviation, airlines, hotels, restaurants, concerts halls, trends in leisure events, theme parks. Travel Industry Keynote Speaker

Quiet Quitters: 50% US workforce wish they were working elsewhere. How engage Quiet Quitters and transform to highly engaged team members. Why AI / Artificial Intelligence is not answer. How to tackle the Great Resignation. Human Resources Keynote Speaker

The Great Resignation. 50% of US workers are Quiet Quitters. They have left in their hearts, don't believe any longer in your strategy. 40% want to leave in 12 months. Connect with PURPOSE to win Quiet Quitters. Human Resources Keynote Speaker

Future of Human Resources. Virtual working, motivating hybrid teams, management, future of motivation and career development. How to develop high performance teams. HR Keynote Speaker

Speed of change often slower than people expect! I have successfully forecast major trends for global companies for over 25 years. Focus on factors driving long term changes, with agile strategies for inevitable disruptive events. Futurist Keynote Speaker

Agile leadership for Better Risk Management. Inflation spike in 2022-3 - what next? Expect more disruptive events, while megatrends will continue relentlessly to shape longer term future globally in relatively predictable ways. Futurist Keynote Speaker

Crazy customers! Changing customer expectations. Why many decisions are irrational. Amusing stories. Lessons for Leadership, Management and Marketing - Futurist Keynote Speaker VIDEO

Chances of 2 people in 70 having same birthday? Managing Risk in Banking and Financial Services. Why the greatest risks are combinations of very unlikely events, which happen far more often than you expect. Keynote speaker on risk management

Compliance is Dead. How to build trust. Reputation of banks and financial services. Compliance Risks. Why 100% compliance with regulations, ESG requirements etc is often not enough to prevent reputational damage

Life's too short to do things you don't believe in! Why passionate belief in the true value of what you are selling or doing is the number one key to success. Secret of all leadership and marketing - keynote for 1100 people in Vilnius October 2021

Future Manufacturing 5.0. Lessons from personal life for all manufacturers - why most manufacturing lags 10-15 years behind client expectations in their day to day life. Manufacturing 4.0 --> Manufacturing 5.0. Future of Manufacturing Keynote

80% of sales are won or lost in 3 seconds, How to grow your business by giving attention to small things that really matter. Future of Marketing, Futuris Keynote Speaker - Pardavimu formule in Vilnius

Trust is the Most Important Thing You Sell. Managing your Reputational Risk - vital lessons for all leaders. How to build trust with key customers and markets. Futurist Keynote Speaker

Truth about Global Economic Crisis: America, EU, China, Emerging Markets - Global Economy Keynote Speaker

Futurist Keynote Speaker: Posts, Slides, Videos - Future Trends, Economy, Markets, Keynote Speaker

“Smart Economics is about more than numbers in a globalised, rapidly changing, digital world.”

It is easy to gain the impression from TV news channels and Business news pages that the entire global economy has been in free-fall for the last 2-3 years, and that recovery is a long way off. Nothing could be further from the truth.

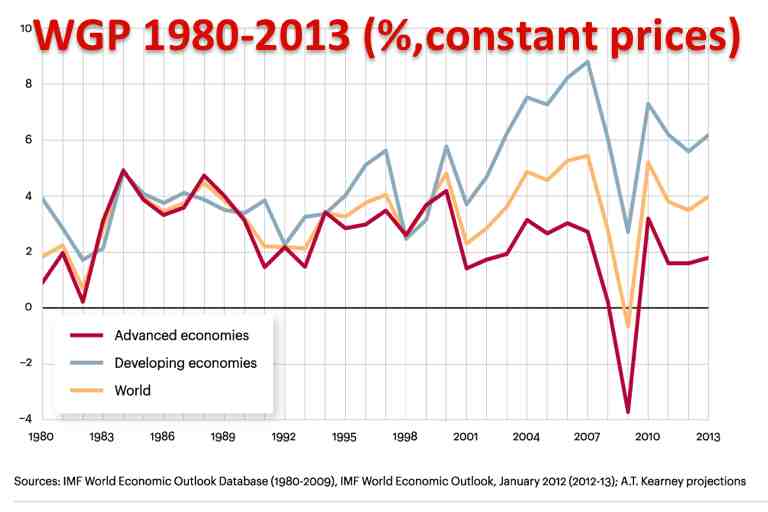

Just look at the graph below – which shows World Gross Product, adjusted for inflation, from 1980 to 2012. Over the 32 year period it is true that we have only seen one dip on the scale of 2009, but look how short it has lasted.

By 2011, GWP had bounced back to levels seen in 2004-2007. The world economy only shrank for just over 12 months.

Recovery was also swift in developing nations – but remember that on average their lowest growth rate was still around 3%, a level that most developed countries would regard as astonishing in the circumstances.

It is true that our world continues to be vulnerable to a further economic shock, but we do need to see these things in the context of longer history, and longer future.

What could trigger second global economic crisis?

What kind of events could trigger a second global shock? The answer is a wide variety. Here are a few scenarios that, while unlikely, could depress GWP by more than 3% for 2-3 years.

1) Iran – US – Israel conflict: that continues beyond a short missile strike, creating huge fear in the markets of wider contagion, and an oil price spike at over $200 a barrel for more than a year.

More likely: limited action, together with severe sanctions, resulting in changes inside Iran.

2) Mutant virus pandemic: similar to Sars or Bird Flu. Remember that with Sars, only 8600 cases and 860 deaths was enough to have a huge impact on international travel and business confidence, especially in all-important rapidly growing Asian nations.

More likely: several new mutants emerge over the next two decades, at least one of which is potentially a major global threat, but is successfully contained by increasingly efficient control measures.

3) Messy break-up of Eurozone: Greece leaves earlier than markets expect, followed by frenzied speculation by investors, betting that Spain, Portugal or even Italy could be forced out in the following 2-4 years. The result is unprecedented spike in borrowing costs for governments of these nations, threats of default on debts, actual defaults, and a complex cascade of debt-related crises in many of Europe’s largest banks.

More likely: Greece leaves the Euro no sooner than 2014, by which time the risks of it doing so have been fully priced into market risks by investors. Stronger structures are in place by then to limit contagion, and the Eurozone muddles through the following years without meltdown, printing money, tolerating slightly higher inflation as a necessary evil to maintain economic and social stability.

But even if there should be second crisis, our world as a whole economic ecosystem is likely to bounce back once more, within 2-3 years.

The reason is that the global economic impact of “globalisation” has yet to be fully felt, coupled with the accelerating impact of technology innovation, and the impact of the digital world.

1) Globalisation

– will continue to drive economic growth for the next 30 years, so long as it is not neutralised by increasing trade barriers, protectionism of all kinds.

Our world is increasingly trading as a single market. This means that nations with low-income labour are able to sell that labour to higher-income nations, in manufacturing and services which are exported such as software or tourism. This will go on happening until higher income nations have slowed growth of wealth to the point where lower income nations have caught up, (assuming that productivity of workers is also equalising gradually in both parts of the world).

Two thirds of the world live in low income nations. One third of the world lives in China and India alone, mostly in very remote places. Over 2 billion more people have yet to join the global economy.

Every year, another 50-80 million people move from remote rural areas in the poorest nations, to their nearest cities, providing a continuous supply of very cheap labour. And every year, another 50-80 million city dwellers move up the ladder of education, work experience, skills and income, to become middle class consumers, adding to the growth of internal markets in these nations.

Globalisation depends on ever-more efficient supply chains, logistics companies, shipping hubs – all of which will be delivered at speed at even lower cost, despite rising energy prices.

2) Technology innovation

– will generate new waves of economic growth, creating industries that do not even exist today. Just look at the last 20 years of advances in the motor industry, in robotic assembly lines, precision engineering, engine design, aerodynamics, computer control. Innovation allows us to do more with less.

We have seen similar revolutions in every area of manufacturing. New materials, new processes, even greater economies of scale. New methods of gas extraction for example have increased proven, usable gas reserves from 60 to 200 years in half a decade, despite increasing use of gas. Prices have fallen dramatically in America, shutting 57 less efficient coal-fired power stations. Similar innovation has meant that solar cells, wind power and other alternative energy sources are also falling rapidly in price to a point where they will soon be economically viable without government subsidy.

3) Digital revolution

– from old-style web to mobile, our world has been transformed beyond recognition over the last two decades. The poorest nations have in some ways been impacted the most. In nations like Vietnam, there are more mobile phone SIM cards than adults.

SMS has revolutionised the ability of remote farmers to judge the precise moment to take their food to market, or the ability of foreign-based workers to send money home to relatives who have no bank accounts.

We are still in the first hour of the first day of the first week of the digital revolution. Future generations will record that it took until 2040 for society to fully maximise the economic impact of smartphone technology that was becoming widespread by 2010.

Summary

So then, it is hardly surprising that the global economy bounced back as rapidly as it did, and barring a global catastrophy, we can expect, on average over the next three decades, at least 2.5 - 3% growth in the global economy, powered mainly by further urbanisation and industrialisation in the poorest nations.

We can also expect many future challenges along the way, with booms and busts in industries and entire nations or regions. Such crises will be more frequent because of increasing complexities that connect markets in unexpected ways. Crises will also be more severe because investor behaviour, influenced by hunch, mood and rumour, now spreads around the entire globe in a matter of minutes or seconds.

So what are your own views? Please do comment below.

| < Prev | Next > |

|---|

Newer news items:

- Life after Brexit: why I was right about immediate impact of the Brexit vote and what next. Why Brexit impact on trade, services, visas, banks and retail sales will be less than many fear

- BUY MY NEW BOOK: The Future of Almost Everything - reprinted twice in last 4 months - or read FREE SAMPLE CHAPTER

- Huge Brexit shock to global economy? Truth about Brexit impact on UK, future of Europe, Eurozone, exchange rates, migration, business and wider world. Predictions written in 2016 and were very accurate. Futurist Keynote Speaker

- Forecasts I made re Brexit were correct: short term and long term. Impact on your personal life, house prices, brexit business strategy, community, EU and wider world. Cut through toxic nonsense. Keynote speaker on geopolitics and economy

- Can a Futurist REALLY predict the future? Here's loads of predictions I made over last 20+ years in 16 Futurist books and as a Futurist keynote speaker

- 5 reasons why every business needs to know about "The Future of Almost Everything" - my latest Futurist book. Discover your Future

- The Future of (Almost) Everything: Impact on Saudi Arabia economy and business. Global Competitiveness Forum - Saudi Arabia Futurist keynote for international investors - VIDEO

- 10 trends that will really DOMINATE our future - all predictable, changing slowly with huge future impact - based on book The Future of Almost Everything by world-renowned Futurist keynote speaker. Over 100,000 views of this post. Discover your future!

- The Future of Almost Everything - 6 Faces of the FUTURE CUBE. Futurist methodology - global trends video

- Future Trends - impact on Baltic Region and Wider World. Interview on Infotech, biotech, Crimea, possible breakup of UK, keys to business success

- Future of the Turkish Economy: Turkey economic outlook, growth, inflation. Futurist Speaker - VIDEO

- Future of Northern Ireland Economy - Growth Strategies

- China as world's dominant superpower - Impact on America, Russia and EU. Futurist keynote speaker on global economy, emerging markets, geopolitics and major market trends

- Truth about UK debt - hidden ways for government to reduce

- Future of Europe - Why EU is splitting into two regions

Older news items:

- Future of Euro – and possible breakup of the EU / Eurozone. Futurist keynote speaker

- How interest rate policies will change: future inflation risks, global economy

- Making sense of the 2007-2015 economic crisis - what next? Look back from 2100 - VIDEO

- Future of Europe - strains and stresses, economy, eurozone

- Sustainable growth - happynomics - key trends

- Trends and Countertrends - Futurist Tools to help predict future

- Take Hold of Your Future - be Futurewise - strategies for growth

- How to grow your business targeting demographics - impact on growth strategy - VIDEO

- Truth about the Global Economc Crisis 2007-15 - looking back from year 2100

- Future Inflation or deflation? Economic Outlook Europe / US

- Future of the Euro crisis in Greece, Ireland. Italy, Spain, Portugal. Eurozone impact.

- Future of the global economy after 'reset' May 2009

- Globalisation: Mergers and Demergers Chaos

- Future of Euro Zone Euro break up. Crisis and what next

- Credit Crunch, Economic Crisis and Possible Recession

Thanks for promoting with Facebook LIKE or Tweet. Really interested to read your views. Post below.

Futurist Keynote Speaker

- Impact of AI on Health Care and Pharma – Artificial intelligence keynote outline for Pharma companies and health care organisations. How will AI drive future AI innovation in health and Pharma?

- Life with AI - my latest book, out soon. How to survive and succeed in a super-smart world. 28 chapters on impact of AI in every industry, government, company, personal lives

- Risk of Russia war with NATO. Russia's past is key to it's military future. War and Russian economy, Russian foreign policy and political aspirations, future relationship between Russia, China, EU, NATO and America - geopolitical risks keynote speaker

- Over 2 million have watched my Green Energy Webinar! "Next 20 years will determine future of humanity": predictions for 40 years. Massive scaling green tech. Race for solar, wind v coal, oil, gas. Climate emergency. Futurist Keynote for Enel Green Power

- How AI / Artificial Intelligence will transform every industry and nation - banking, insurance, retail, manufacturing, travel and leisure, health care, marketing and so on - What AI thinks about the future of AI? Threats from AI? Keynote speaker

- The Future of AI keynote speaker. Will AI destroy the world? Truth about AI risks and benefits. (Some of this AI post written by AI ChatGPT - does it matter?). Impact of AI on security, privacy AI, defence AI, government AI - keynote speaker

- Future of Rail in 2030: trends in rail passengers, rail freight, railway innovation. High speed rail, impact on aviation. Rail logistics and supply chain management. AI impact, Zero carbon hydrogen powered railway locomotives - Rail Trends Keynote

- Future of the Auto Industry 2040. Trends impacting the auto industry, car manufacturers, truck factories. Auto industry innovation, autonomous vehicles, flying cars, vehicle ownership, car insurance AI / Artificial Intelligence.Futurist Keynote for Belron

- Future of Aviation: Carbon Zero Planes. New fuels such as hydrogen, smaller short distance battery powered vertical take-off vehicles. Why Sustainable Aviation Fuel is not the answer to global warming. 100s of innovations will transform aviation eg AI

- THE TRUTH ABOUT FUTURE MASS MIGRATION - a people movement with greater force than any military superpower. As I predicted in "Futurewise" (1998-2005), large scale migration is now unstoppable, able to break governments, yet many nations NEED migration

- Why MOST CEO SPEECHES don't create passion or purpose - just create Quiet Quitters. 270,000 views of this PURPOSE speech which no AI can deliver. For typical company in an industry often criticised. Reverse Great Resignation! Leadership Keynote Speaker

- The Future of Life Insurance. Why life insurance will boom globally. New pattens for selling life cover, AI automated underwriting , wearable devices, dynamic premiums. How life expectancy will change.How to build your brand.Life Insurance keynote speaker

- Future of Leadership and Management, Human Resources, Virtual Teams and AI, Hybrid Working, Offices, Quiet Quitting, Careers, Team Motivation, Attracting Talent, Team Engagement - Workplace Keynote Speaker

- Back to Work! Face to Face Meetings Win New Business, Accelerate Innovation, Increase Agility, Implement Change. Future Offices, Future of Work and Workplace in world of AI. Working from Home (WFH). Artificial Intelligence impact on Work

- Future of Retail Globally - why scale matters for lower cost, better products, stronger brand. Future retail growth in every region of the world will follow same patterns. 70% of retail is 8 companies in the UK. Retail Keynote Speaker

- Queen Elizabeth II: the power of example over a lifetime. Lessons for all great leaders. Why her impact on our future world will be so long lasting. Example is the only form of leadership that endures, because it is based on integrity and authenticity

- Future HR trends, workplace, rapid reversal of % time working from home, office occupancy, motivation, recruitment and leadership in an AI world.How to form most effective teams and why most change management strategies fail. HR keynote speaker interview

- Race towards Net Zero Emissions will happen MUCH faster than most predict, accelerated by Russia's war, rapidly falling prices for green energy, innovation, AI and growing global anxieties about climate emergency. Sustainability keynote speaker VIDEO

- 90% of global trade will continue to be container shipping. Cities with large container ports will continue to be hubs for manufacturing, logistics and supply chains for the next 100 years. Future of logistics and supply chain keynote speaker VIDEO

- Small things often have the greatest impact for customers, often cost very little or can even save huge amounts of cost. Logistics and supply chain example - fill empty trucks on return runs (40% of all road freight). Futurist Keynote Speaker VIDEO

- 7 keys to success in logistics and supply chain business. Summary of "Future of Logistics and Supply Chains" Keynote by Patrick Dixon, Futurist Keynote Speaker for Seminarium, Chile - VIDEO

- Q+A: Future of the Food Industry in Latin America, impacted by huge rise in freight costs? When all container freight costs return to normal? Logistics keynote speaker at Seminarium Santiago - VIDEO

- How to Communicate Bad News to Customers. Crisis management - example from logistics and supply chains disruptions. TRUST REALLY MATTERS. Act FAST, be transparent, keep clients updated, work together to find solutions. Logistics keynote speaker

- Q+A: How LITTLE THINGS often create client magic for your VIP customers and clients. Example from supply chains and logistics. Beyond anything that AI / Artificial Intelligence will deliver for your business. Create MAGIC. Futurist Keynote speaker VIDEO

- Q+A Keys to Agile Leadership. Why timing is EVERYTHING in a crisis, backup plans, contingencies, alternatives, dynamic strategy. Lessons on Agility and Agile Leadership from recent disruptive events. Logistics and Risk Management Keynote Speaker

- Q+A What about Future of Logistics in Banking? Dealing with costs of cash handling, and alternative beyond mobile payments. Comment on future of BlockChain, Cryptocurrencies, BitCoin etc - issues of sustainability and efficiency. Banking Keynote Speaker

- Q+A: Future costs of freight? When will container shipping costs fall to normal? Reasons for supply chain crisis. Predictions for future cost of shipping. Future of Logistics and Supply Chains Keynote Speaker

- Q+A: Future Logistics and Supply Chains - outsource or in-house logistics and supply chain teams? Look for growth in Virtual Logistics operations / AI combining agility and scale with control and visibility - Future of Logistics Keynote Speaker VIDEO

- Future energy prices and investment? Future energy markets (oil, gas, coal, nuclear power, wind, solar power etc) will be driven by EMOTION not just "market forces". Examples from recent disruptive energy-related events. Energy trends keynote speaker

- Q+A How to tackle shortage of truck drivers. Why truck driver crisis really matters and how too solve it. Road freight trends. Seminarium: Logistics Supply Chain Keynote Speaker - VIDEO

- 10 seconds to Win the Customer! How to Make Magic for Future Retail Customers in an omnichannel world. And why location is the most important fact you need to know about your customer NOW. Futurist keynote speaker on Future of Marketing

- Russian military strategy in Ukraine under pressure. Longer term impact of military action / war on energy industry, wider economy and other geopolitical risks. Patrick Dixon is a Futurist Keynote Speaker

- Emerging markets will drive global economic growth for next 60 years - where 85% of humanity lives. Global Economy and Macrotrends Keynote Speaker

- Future of the Travel Industry post COVID. Bounce-back as I predicted for Aviation. What next for tourism and business? Why the travel industry will be an engine of global economic growth. Impact of AI. Travel industry keynote speaker at Seminarium event

- COVID, Russia, Energy Crisis, inflation spike, interest rate rises, AI impact on society - how many more shocks can we expect? What next? Interview with Futurist Keynote Speaker and Trends Analyst - Patrick Dixon

- Energy as a national security strategy. Added incentives to go green. Futurist view of Future of the energy industry, oil, gas, coal, solar and wind in a post-COVID world impacted by regional conflict

- Future of Global Trade, Logistics and Supply Chain Management- agility and risk. Scandal of empty containers and boom in regional trade v global. Reducing supply chain risks and disruptions from more global events like the COVID pandemic - keynote speaker

- Future Flying Taxis? Impact of AI on Future of Urban Air Mobility driven by over 250 new companies - electric vertical takeoff and landing (eVTOL). Impact of eVTOL on the future of the aviation industry. Aviation trends Keynote Speaker

- 10 steps to Agile Leadership in a Crisis. Keys to Agile Business Strategy in uncertain times: Turn market chaos into opportunity. Take Hold of Your Future. Leadership keynote speaker

- Managing MAJOR RISKS, economic shocks, pandemics, geopolitical, disruptive tech like AI. Reduce RISKS with agile leadership. Risk management in banking and why many banks are blind to combined impact of different events - risk management keynote speaker

Most Read - Futurist Speaker

- Conference Speakers: How Great Conference Speakers Change Lives. 10 tests BEFORE booking top conference speakers. Keys to world-class events. Secrets of ALL best keynote speakers. Who are the best keynote speakers in the world? 327,000 views of this post

- Futurist Speakers: How keynote by Patrick Dixon will transform your event. Visionary, high impact, high energy, entertaining Futurist keynotes on future trends. Keynotes on AI, tech, health, marketing, manufacturing etc. 315,000 have read this post

- Future of Marketing 2030 - Marketing Videos, key marketing trends and impact of AI on marketing campaigns. Conference Keynote Speaker on Marketing - 232,000 have read this post

- The Future of Outsourcing in world beyond AI - Impact on Jobs - Futurist keynote speaker on opportunities and risks from outsourcing / offshoring. Why many jobs coming home (reshoring - shorter supply chains). AI and new risk, higher agility. 200000 views

- Futurist Keynote Speaker Website - Sorry - something has gone wrong! We will check it out...

- Future of Stem Cell Research - Creating New organs and repairing old ones. Trends in Regenerative Medicine, anti-ageing research, AI. Future pharma, clinical trials, medical research, heath care trends, and biotech innovation.Health care keynote speaker

- Future of the European Union - Enlarged or Broken? What direction for the EU over the next two decades? Geopolitics keynote speaker

- 10 trends that will really DOMINATE our future - all predictable, changing slowly with huge future impact - based on book The Future of Almost Everything by world-renowned Futurist keynote speaker. Over 100,000 views of this post. Discover your future!

- Future of the Automotive Industry (Auto Trends) - e-cars, lorries, trucks and road transport trends, reducing CO2 emissions, e-cars, eVTOL flying vehicles, hydrogen, autonomous AI drivers, auto industry impact from AI. Futurist keynote speaker

- The Truth About Drugs - free book by Dr Patrick Dixon - research on drug dependency, addiction and impact on society of illegal drugs

- Forecasts I made re Brexit were correct: short term and long term. Impact on your personal life, house prices, brexit business strategy, community, EU and wider world. Cut through toxic nonsense. Keynote speaker on geopolitics and economy

- Marketing to Older Consumers - 1.4 billion over 60 year old consumers by 2030. Future of Marketing Keynote Speaker. Ageing customers, strategies to target older consumers and other marketing trends. Why many companies fail in marketing to older people

- Future of Aviation Industry. Rapid bounce back after COVID AS I PREDICTED. Most airlines and airports were unprepared for recovery. Aviation keynote Speaker. Fuel efficiency, reducing CO2, hydrogen fuel, AI, zero carbon, flying taxis (eVTOL)

- China as world's dominant superpower - Impact on America, Russia and EU. Futurist keynote speaker on global economy, emerging markets, geopolitics and major market trends

- Web Traffic: Up to 2.9 million pages a month - Future Trends website of Patrick Dixon, Futurist Keynote Speaker

- Futurist Keynote Speakers. 20 secrets of world's best keynote speakers. How to select great keynote speakers for your events. Secrets of all top keynote speakers. Change how people see, think, feel and behave. Who are the best?

- Future of Insurance 2030. Insurance industry trends keynote speaker. How insurance customers are changing. Why insurance marketing, AI underwriting and claims handling will change radically. Most important growth markets for insurance products

- Designer babies - how biotech can help parents create a 'perfect' child - huge ethical questions about the future of human race. Pharma trends and Future of Biotech Keynote Speaker

- Technical Setup for Futurist Keynote Speaker Patrick Dixon

- Total audience reach >450 million on TV, Radio, Press Coverage of Patrick Dixon, Futurist Keynote Speaker

Outsourcing is destroying America as it only serves the 1% at the expense of the rest of us.